A View on: Figures and market data from France

Franceclat recently released market data for the French watch and jewelry industry for 2025. Let’s take a look across the border:

About Francéclat

Francéclat is a semi-public organization dedicated to promoting the French watchmaking, jewelry, and tableware industries. It is funded by approximately 14,000 companies in the sector and serves as a central platform for market research, industry development, and international positioning. Its responsibilities include analyzing market data, supporting companies in their transformation and innovation efforts, and promoting French creative industries both domestically and abroad – www.franceclat.fr

Between Stability and Change

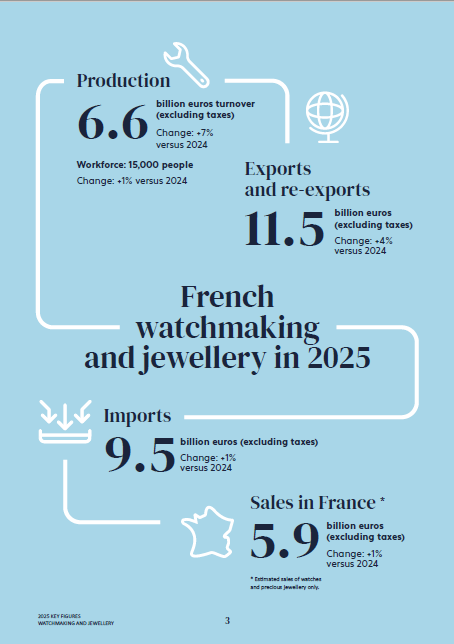

The latest figures from France paint a mixed picture of the watch and jewelry industry. At first glance, the market appears stable: total sales stand at around 5.9 billion euros, slightly higher than last year and significantly above 2019 levels. Yet behind this apparent continuity, the balance of power is shifting noticeably.

Jewelry is pulling ahead

The trend in the jewelry segment is particularly striking.

With a production volume of over 6 billion euros and growth of 8 percent, the positive trend of recent years continues. This development is driven almost exclusively by the high-end segment—particularly gold and platinum jewelry.

At the same time, the price-sensitive segment is losing ground. Costume jewelry and gold-plated items are on the decline, while the market is clearly shifting toward quality and substance.

The watch industry, on the other hand, presents a different picture. While exports remain stable and mechanical watches continue to dominate by a wide margin, growth is moderate. The momentum clearly lies with jewelry.

Value over volume

A key driver of this trend is the sharp rise in precious metal prices. Gold, silver, and platinum have risen significantly in 2025—with direct implications for the market.

The result: rising sales despite a decline in unit volume. Growth is driven less by demand volume than by price trends and higher product values.

This shift is also changing consumer behavior. Jewelry is increasingly seen not as a fashion accessory, but rather as an investment with lasting value.

Return to brick-and-mortar retail

At the same time, there is a clear shift in sales channels. While brick-and-mortar retail is growing slightly, online retail is seeing a significant decline. In the jewelry segment in particular, the physical experience—materials, craftsmanship, and texture—appears to be regaining importance.

Specialty retailers are maintaining their position, while traditional mass-market channels are coming under pressure. The market is becoming increasingly differentiated—not only in terms of products, but also in terms of distribution.

Thus, the situation in France in 2025 was not unlike that in Germany.

What does this mean for German industry?

If one looks solely at import and export figures, it becomes clear that Germany, with its nearly balanced trade balance in jewelry, can be viewed more as a trading hub in which foreign producers also play a role. This is also clearly evident when looking at the windows of jewelry stores.

In the European context, the German jewelry industry thus occupies an intermediate position: it has a solid production base consisting mainly of small and medium-sized enterprises, but does not achieve the industrial scale and depth of value creation found in countries such as Italy or France.

Its strength therefore lies less in large-scale, high-end production and more in technical expertise, trade, and market size. Germany is thus neither a leading production hub nor a purely consumer market, but occupies a middle ground between the two.

This has two consequences:

- Competition is becoming fiercer, faster, and more direct

- At the same time, there is growing pressure to define one’s own areas of expertise more clearly

German companies, which have traditionally excelled in technology, precision, and industrial manufacturing, now face a strategic question: Is product quality alone enough—or is stronger differentiation through branding, design, and communication needed?

This question is all the more relevant now, especially given the current situation, in which nothing seems certain, markets are collapsing, new crises are emerging, and there appears to be no domestic momentum left.